MarketsMuse.com Options market update focuses on recent industry report canvassing the perch of buyside managers perspective as to the good, the bad and the ugly sell-side broker elements they encounter in the course of increasing use of listed options products is courtesy of recent report issued by industry think tank, TABB Group.

Not surprisingly, buy-side managers canvassed in this study (including traditional managers and hedge fund managers) found that execution quality is paramount, particularly as market structure evolves and fragmentation rises, more important, the fact that liquidity from traditional ‘capital commitment’ desks–and the ease in which an institutional customer can execute “on the wire” is diminishing for all but most favored-clients.

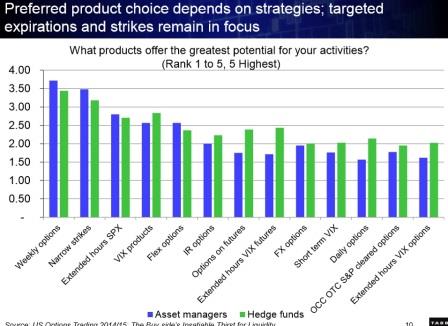

The TABB study provides further insight as to which option products are of the greatest use to managers, the importance of algos vs. the importance of research and the most important ‘value-adds’ that sell-side brokers can contribute.

MarketsMuse.com update courtesy of coverage by TheStreet.com

Investors should avoid the Utilities Select Sector SPDR ETF (XLU) despite the recent dovish talk by Federal Reserve Chair Janet Yellen, said Mohit Bajaj, Director of ETF Trading Solutions at WallachBeth Capital. Bajaj added that rising rates will hurt the XLU because power companies are levered to debt financing which will become more expensive. He is also bearish on the SPDR Barclays High Yield Bond ETF (JNK) due to the potential for rising rates and problems in the energy sector. On the other hand, Bajaj is bullish on the Financial Select Sector SPDR ETF (XLF) because the large-cap banks will benefit from rising rates and have passed their stress tests. Below is the video interview..

MarketsMuse blog update courtesy of extract from 27 Feb story from ETF.com’s Elisabeth Kashner and her profile of prop trading firm Virtu, the high-frequency (HFT)“Virtu’s HFT Way To Play Crazy Oil Market”

Elisabeth Kashner, ETF.com

Would you ever sell something to yourself and pay someone else to be the middleman? Nobody’s that dumb, right?

Virtu, the high-frequency trading firm (HFT) of the type profiled in “Flash Boys,” did just that, to the tune of $32 million.

High-frequency traders are perhaps the most sophisticated players on Wall Street. Some might be scoundrels, but they’re not fools. That’s why their recent trades in oil futures-based ETFs are so fascinating.

Like hedge funds and mutual funds, HFT firms keep their portfolios under wraps, except when the Securities and Exchange Commission requires disclosure.

Virtu’s most recent form 13F, the Securities and Exchange Commission’s quarterly holdings report, revealed a $46 million position in United States Oil (USO | B-100) at the close of business on Dec. 31, 2014. USO buys front-month oil futures. By the end of 2014, with oil prices at a 10-year low, USO shares had taken a beating, as you can see in the chart below. Continue reading →

MarketsMuse update inspired by yesterday’s column by Tom Lydon/ETFtrends.com and smacks at the heart of what certain “bomb throwers” believe could be a Black Swan event, albeit an event that may not be driven by a global crisis or surprise economic event. The event in question will, in theory, take place when interest rates start ticking up (and underlying corporate bond prices tick down) and institutional bond fund managers find themselves trying to figure out whether to simply suffer from mark-downs (and performance) or to continue collecting coupons until the issues they hold mature.

MM Editor Note: Since most folks know that bond managers are akin to lemmings (no disrespect intended!) and typically follow each other like blind mice, given the massive size of the corporate market place, a potential avalanche could take place when everyone runs for the exit if rates tick up and simultaneously, the economy starts to slow. Wall Street dealers are certainly not going to be available to catch those falling knives, simply because new regulations have put a crimp in the capital they can commit to warehousing positions. Worse still, its easy to envision one very long contango event, where the cash ETF trades at a discount to the value of the underlying bonds, simply because one won’t be able to sell those underlying bonds in any type of material size.

Here’s an opening extract from Tom Lydon’s piece “Liquidity Concerns In Corporate Bond ETFs”: Continue reading →

MarketsMuse.com update courtesy of extract from Feb 16 CNBC reporting by Alex Rosenberg

Alex Rosenberg, CNBC

There’s a major debate brewing in the financial markets, and it concerns the most important potential event of the year for stocks and bonds alike: the timing of a Federal Reserve rate hike.

In one corner are the economists. Many of those looking primarily at the state of the recovery say that the Fed will likely raise its key federal funds rate in June.

On the other side are traders, who say that current market dynamics—and prior experience with the central bank—tell them that a rate hike isn’t coming in 2015.

What the Fed actually chooses to do, of course, will have a profound impact on financial market, and perhaps on the economy as well. The federal funds rate, a critical short-term rate at which banks can lend to one other, has been kept ultra-low by the Fed since the financial crisis days of December 2008.

Now, many economists expect that the Fed is finally set to shift from ultra-low levels, given the strong state of the labor market.

With the unemployment rate declining and payrolls data showing some 250,000 payroll gains a month, “the U.S. labor market is screaming for policy normalization,” as Societe Generale economist Aneta Markowska put it in a recent note.

If the economists are right, a hint at a June rate hike could come as soon as Wednesday, when the Fed will release the minutes of their last policy meeting. If the minutes find them gushing about growth and unbothered by economic and geopolitical problems overseas, it could serve as a reminder for investors that a June hike is still on the table. So, too, could the congressional testimony of Fed Chair Janet Yellen in the following week.

The Fed is “much closer to hiking then putting it off,” said Neil Azous of Rareview Macro, a firm that advises large investors. After all, “it is hard to argue from an economist’s perspective that they shouldn’t at least start the process. Their models are telling them to, regardless of the problems abroad in Europe and Asia.”

Strong job creation, especially if February’s payrolls top expectations, could also hint at a tightening. “If the job market holds anywhere close to what it’s been running at, then yeah, we’ll get a hike,” agreed Deutsche Bank economist Joseph LaVorgna. “I don’t see why the Fed wouldn’t go in June.”

Still, that sentiment is clearly not reflected in the market. Fed funds futures are implying just a 20 percent chance of a rate hike in June, according to CME Group’s FedWatch tool.

Indeed, if Yellen does give a hint in the weeks ahead that a June rate hike is possible, “the fixed income market would re-price swiftly and painfully against the consensus long position,” Azous said.

In other words, rates (which move inversely to bond price) could rise dramatically. And that, in turn, could have a profoundly negative impact on stock prices. Continue reading →

MarketsMuse blog update courtesy of extract from news report by Reuters’ Ashley Lau

State Street Corp said on Tuesday it has slashed management fees on 41 of its SPDR exchange-traded funds, joining major ETF providers BlackRock Inc and Vanguard in their efforts to lower fees as price competition heats up.

The price cuts at State Street, which affect a range of international and domestic equity and bond funds, come at a time when cost has become an increasingly important factor for ETF providers. Vanguard, which recently surpassed State Street to become the No. 2 U.S. ETF provider, has been winning assets with its razor-thin fees.

With the new price reductions, State Street’s SPDR Barclays Aggregate Bond ETF, for example, now has an expense ratio of 0.1 percent, down from 0.21 percent. That brings the fund closer to the range of the Vanguard Total Bond Market ETF and the iShares Core U.S. Aggregate Bond ETF, which both have an expense ratio of 0.08 percent.

State Street said the fee reductions are part of an ongoing review process “to identify improvements that are beneficial to investors.”

“Competitive pricing is a core benefit to the SPDR ETF value proposition,” said James Ross, global head of SPDR ETFs at State Street Global Advisors, the company’s asset management business.

ETF assets have been flowing into Vanguard, long a leader in low fees. It increased its U.S. market share to 21.3 percent at the end of 2014, more than doubling its market share since 2008.

BlackRock, the largest ETF provider, has also been expanding its “iShares Core” lineup of low-cost ETFs, a program it started in October 2012 to compete with cheaper funds offered by other providers. The company said on Monday it would extend a partial fee waiver of annual management fees on certain iShares funds in Canada. (Reporting by Ashley Lau; Editing by Dan Grebler)

MarketsMuse provides below extracts from Feb 2 edition of Rareview Macro’s Sight Beyond Sight as a courtesy to our readers. The entire edition of today’s SBS newsletter is available via the link below.

Neil Azous, Rareview Macro

Professionals Taking Move in Crude Oil Seriously…Concern Over Deeper Move Lower in Risk

No One Prepared for Deflation Risk to Subside

Left Tail Risk: Removing Two Key Peg Break Conversations (for today)

China-Korea-Japan Battle – KRW/JPY Hedge

Switzerland – Update

Model Portfolio Update – January 30, 2015 COB: -0.33% WTD, -0.88% MTD, -0.88% YTD