While high-yield bond followers are seemingly caught between a rock and a hard place as interest rates may be poised to pick up, some expert investors are positing that high yield positioning is precisely the tactical approach to maintain.. The following MarketsMuse.com fixed income fix is courtesy of contributed article “5 Reasons to Hold High Yield” from Philadelphia-based RIA Clark Capital Management Group’s Chief Investment Officer, Sean Clark, CFA.

Editor Note: Before any MarketsMuse followers pooh-pooh the notion that spreads are bound to widen (and in turn, disrupting HY bond exposure), Clark Capital has been successfully navigating fixed income markets since 1986 and currently has $3billion AUM. The firm recently launched Navigator® Tactical Fixed Income Fund.

“The high yield market was bloodied in the second half of last year, primarily due to the collapse in energy prices.While yields and spreads backedup,broader-based credit remained firm, suggesting that it was an isolated problem due to the collapse of the energy market.We believe that the high yield market will reward investors who adopt a tactical approach.Below are five reasons we anticipate a reemergence of opportunities in the high yield space in 2015:

- Credit Spreads Offer Value

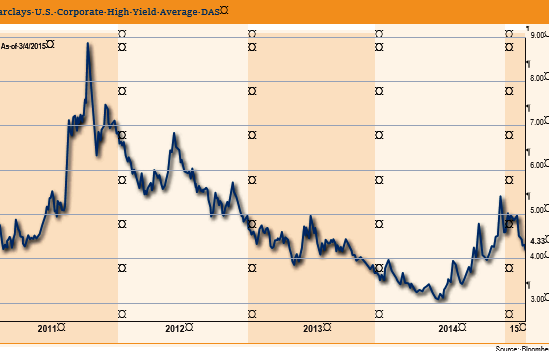

After a solid year for Treasuries and sub-par year for high yield bonds in2014, credit risk seems to be priced for a recovery as the strengthening economy offers support to lower quality fixed income.In mid-December,credit spreads widened to their highest levels since late2012.Credit spreads moved from 222 to 525 basis points,up 136%. That compares to a rise of 138% during the U.S. debt showdown in 2011.The outsized move in spreads set up a nice entry point into high yield.

After a solid year for Treasuries and sub-par year for high yield bonds in2014, credit risk seems to be priced for a recovery as the strengthening economy offers support to lower quality fixed income.In mid-December,credit spreads widened to their highest levels since late2012.Credit spreads moved from 222 to 525 basis points,up 136%. That compares to a rise of 138% during the U.S. debt showdown in 2011.The outsized move in spreads set up a nice entry point into high yield.

For your reading ease of the entire thesis from Clark Capital, please click the image below to launch the opinion in .pdf format.