“What Goes Up, Must Come Down”

MarketsMuse ETF update is courtesy of a special trade post sent this afternoon to subscribers of “Sight Beyond Sight”, the global macro trade newsletter published by Rareview Macro LLC and authored by Neil Azous. The trade alert was also posted to Twitter via @RareviewMacro. For those not familiar with the concept of mean reversion, the simplest metaphor that drives the following thesis is “what goes up must come down.”

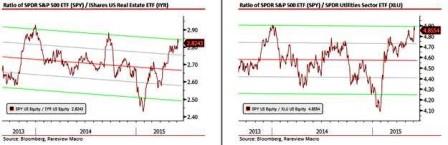

As highlighted in this morning’s edition of Sight Beyond Sight, the ratio of the iShares U.S. Real Estate ETF (IYR) and Utilities Select Sector SPDR Fund to the SPDR S&P 500 ETF Trust (SPY) is now trading at approximately two standard deviations away from its regression line since US interest rates peaked in September 2013.

A short while ago in the model portfolio, we initiated a new mean reversion strategy in both of these ratios.

Specifically, we are buying $10 million notional each of IYR and XLU, and selling $20 million notional of SPY over the rest of today at VWAP.

Tomorrow, depending upon the results of the US Labor Report, we will add an additional $10 million notional each of IYR and XLU, and sell an additional $20 million notional of SPY in the morning.

Below is a thesis and trade matrix with a pre-defined game plan for gains and losses.

Thesis

Currently, US 10-year real yields are now near their highest level for the past 18 months at +50 bps – largely as a result of the recent move higher in European yields. As we have discussed previously, higher real rates are not a positive for equities in the current environment as higher multiples and earnings are predicated on stock buybacks and other financial engineering, especially given that overall S&P 500 sales growth is declining.

As a result, the last two times the ratio of IYR and XLU to SPY reached these extreme levels, which were coincidentally short-term peaks in long-term US Treasury yields, equities also corrected by at least 6% in both instances from peak to trough. These ratios generally expose us to that view.

Because we are already have on a significant amount of long US interest rates exposure, we felt compelled to explain the correlation in the model portfolio. Our Bund-UST relative value strategy is effectively delta neutral. Our Eurodollar futures risk premium strategy has risk to a bear steepening of the yield curve, but benefits from both theta decay and aggressive roll down. Lastly, our position in March 2016 Eurodollar future (EDH6) has the duration of a 2yr note, but benefits from aggressive roll down. The new positions added today have different characteristics.

First, IYR has the highest sensitivity to a constant maturity 20yr bond. Second, XLU has the highest sensitivity to a constant maturity 10yr note. What that means is that these are effectively directionally sensitive to the long end of the US yield curve.

As a result, from an interest rate perspective, ultimately we are adding outright directional exposure in the long end of the US Treasury curve relative to US large cap equities, with a very defined risk profile.

Given the juncture of the US fixed income market and the positioning, we feel this “back door” exposure is a more optimal way to express the same view, both in terms of risk management and correlation.

To read the entire trade strategy proposal and the details therein, please visit the Rareview Macro website (subscription is required; free trial subscriptions are available).