MarketsMuse dip and dash department frequently prefers spotlighting altruists and do-gooders, including Agency-only execution firms in the brokerdealer sphere who, unlike “principal trading desks”, do not take the contra side to institutional customer orders as a means of making a profit; agency-only firms merely execute those client orders via the assortment of major exchanges and dark pools that traffic in equities and equity options. Today’s spotlight is on Dash Financial; the only position they purportedly take is a business model position by promoting the fact they act as a conflict-free agent only representing the best interest of their institutional brokerage clients in consideration for an agreed-upon commission.

The phrase “Best Execution” is therefore popular jargon among agency-only firms and implies that customers are receiving ‘the best” execution. What that means is a function of who you ask, particularly when considering the brokerdealer community has proven uniquely adept at capturing hidden revenue via rebate schemes in consideration for orders routed to those respective venues for execution. These schemes are aggressively promoted by the nearly two dozen major exchange and dark pools that facilitate trading in equities and equity options.

Courtesy of our friends at FierceFinance, today’s altruist of the week award goes to equity and options market agency brokerage Dash Financial, who asserts that being a broker in today’s fast-paced market is about being a technology expert and a consultant on clients’ execution objectives.

“Everything is a tradeoff,” said David Karat, chief marketing officer for Dash Financial. “Every action you take to minimize fees, you risk losing liquidity, and for every technique to maximize liquidity it will cost you more money because it will be less relevant which venues you go to get that liquidity. It’s that balance we sit on top of and consult with our clients on.”

To that end, Dash Financial aims to help clients achieve what it calls on best net execution – execution that incorporates exchanges fees and all other associated costs.

“If there is liquidity in multiple places we are going to capture that liquidity based on the cheapest economics for the client,” Karat said. But Dash Financial has also designed its tracing architecture to couple its best execution algorithms with a focus on in-depth transparency, Karat said.

“We actually want you to see all the child orders, the millisecond time stamp of which destinations we are going to and what happened,” Karat said.

Looking at an example of a client order to sell 1000 Apple May 106 puts at seven cents, Karat notes that the system not only shows that the parent order was filled, but allows clients to click through to see all the child orders associated with that parent order.

In the Apple example, there were actually 828 contracts available to satisfy the order, divided between two different venues. Dash Financial’s platform is calibrated to account for slight differences in the amount of time it takes for orders to reach different venues, and that calibration readjusts during the day as timing slows down or speeds up. After capturing all 828 orders, the millisecond that the system realized a balance remained, it reversed and posted the balance of the order to Arca, because Arca has the best rebates. The order on Arca was hit immediately.

The Dash Financial interface not only allows clients to see the child orders, but through a tool called Order Trace, clients can view everything including FIX messages sent down to the exchange for a complete audit trail for compliance purposes. In addition, a tool called a Smart Order Router Analyzer allows clients to view what Dash saw on screens at the time or the order.

Dash Financial sees its role as using its tools for visibility into execution to work with clients fine tune trade executions to fit the nuances of their strategy.

“What we do is look at that behavior when they are executing and we might say, in this type of scenario, it might make sense to be a little more aggressive, or a little less aggressive and this is what we suggest,” Karat said. “We will go back and redesign how the algorithm behaves in a certain situation or we will give them another algorithm for a specific nuance, and compare it against existing behavior so we can quantify whether it is worth changing again or keeping as it is.”

As reported previously by MarketsMuse, actively-managed ETFs, aka AMETFs (or as Eaton Vance has dubbed their product: “NextShares ETMFs”) are the next holy grail for Issuers of exchange-traded funds simply because these new-fangled products offer a refreshing new batch of flavors to a product category that has nearly 2000 issues whose structures are pretty much the same and all are intended to compete with traditional mutual funds. Eaton Vance is a pioneer in actively-managed exchange-traded funds, and Precidian Investments is biting on their heels so far with their proposal for “ActiveShares”. The difference between the ‘actively-managed’ types vs. the plain vanilla ETFs is total lack of transparency; investors in actively-managed ETFs do not know what the underlying components are, so the value proposition is presumably based on the ETF managers’ capabilities.

For some, actively-managed ETFs are the perfect product for hedge fund operators to promote, given that hedge fund investor appeal for investing in hedge funds is the secret sauce each of them purportedly uses to make profits for investors, or per industry jargon, “capture Alpha.”

For ETF market-maker veterans, the notion of not knowing what the underlying components are is counter-intuitive. Unlike a traditional, single stock specialist who makes a two-sided market in IBM, and is willing to either buy or sell based on their ability to gauge which direction the stock is headed next, ETF market-makers don’t take that kind of risk, they make money by providing a two-sided aka bid-offer market in any particular ETF based solely on their ability to arbitrage the underlying components vs. the cash price of the ETF. In simple speak, an ETF market-maker is only interested in offering 50,000 or more shares of the ETF if they can simultaneously purchase the underlying constituents of that ETF at an aggregated price that is less than the current offering price of the ‘parent’ ETF. They will only make a bid for a block size trade if they think they can simultaneously sell-short the underlying constituents such that the aggregate ‘sale price’ is greater than the price they pay for the cash ETF product.

Irrespective of whether actively-managed ETFs can prove to be liquid trading vehicles, which is arguably a criteria for most investors, NextShares non-transparent product has been approved by the SEC, while its competitor, Precidian Investments continues to face hurdles with the regulators. Perhaps this is a who-you-know issue. As noted by WSJ’s coverage by Daisy Maxey:

Regulators denied a second request from Precidian Investments for approval to launch actively managed exchange-traded funds that wouldn’t have to disclose their holdings daily, as ETFs now do. The latest SEC denial of Precidian’s ETF plan “ActiveShares”became public Monday when competitor Eaton Vance posted it on its website. In October, the SEC denied Precidian’s filing for a nontransparent active ETF that would trade on an exchange. Precidian refiled with the regulator in December after making changes, seeking exemptive relief to launch its funds, which it called ActiveShares.

But in a denial letter dated April 17 that just become widely available, the SEC notes that it had previously denied a “substantially similar” proposal from Precidian.

Daniel McCabe, chief executive at Precidian, said the company is in a “fruitful” and ongoing dialogue with regulators, and plans to refile to launch the funds.

The latest SEC denial of Precidian’s ETF plan became public Monday when competitor Eaton Vance Corp. posted it on its website. Eaton Vance, which has received SEC approval to launch a related product called exchange-traded managed funds, said it obtained the SEC communication to Precidian through a Freedom of Information Act request. Precidian’s product would have been a competitor to the ETMFs planned by Eaton Vance.

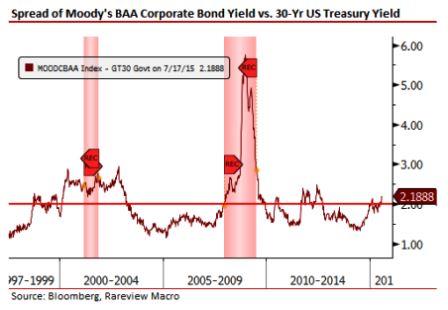

MarketsMuse Global Macro and Fixed Income desks converge to share extract from 23 July edition of Rareview Macro commentary via its newsletter “Sight Beyond Sight”. For those not following the corporate bond market, most experts will tell you the equities markets follow the bond market–which in turn is a historical indicator when it comes to economic expansion, contraction, and recession. Below is courtesy of Rareview’s founder/managing member Neil Azous .

In the past few days, US investment grade (IG) credit spreads have reached new three year wides. Historically, the absolute level of these spreads is consistent with periods of economic and financial market stress. Additionally, the daily volatility of these spreads has increased dramatically in recent weeks.

Below is a chart of the Moody’s Baa Corporate Bond yield spread over the US 30-year Treasury yield.

What is the significance of this observation?

Investment grade corporate bonds are one of the least risky investments within the capital structure, and less sensitive to changes in default risk due to economic weakness. Moreover, the credit market is arguably, next to the slope of the yield curve, the greatest predictor of future economic stress.

The most widely cited explanation for the recent widening in spreads is that it is due to the amount of new investment grade credit issuance. Indeed, that is one factor as new issuance (+SSA) set a record pace yesterday after having surpassed $1 trillion, a level not reached last year until mid-September.

However, the recent widening of the spreads is not just down to the recent surge in corporate issuance. Issuance is simply not a large enough driving force to cause this level of “stress”. The reasons for this widening are two-fold.

Firstly, the aggregate level of issuance, to a degree, is beginning to finally catch up with the market after years of sensational appetite. Corporations, in aggregate, are raising their leverage levels by issuing the new debt and not using the proceeds to grow their revenues or cash flows to compensate. Put another way, the market is beginning to segregate between issuance related to refinancing a company’s “credit stack” as part of its normal annualized funding requirements and pure capital redeployment for the benefit investors.

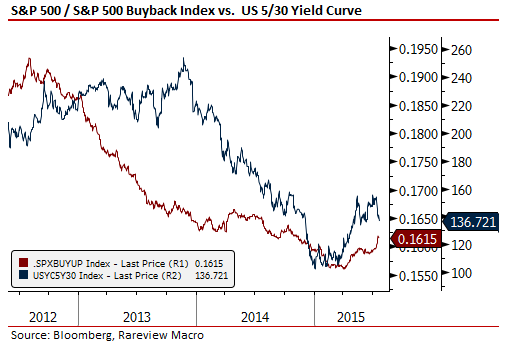

By the way, as we have pointed out in these pages for a while now, not only is the IG spread widening, signaling the distinction noted above, but the equity markets are now doing so as well. Again, see the below chart of the ratio of the S&P 500 to the S&P 500 BUYUP index overlaid with the US Treasury 5-30yr yield curve. Stock buy-backs are simply underperforming in 2015 after multiple years of outperformance as the yield curve steepens in anticipation that interest rate hikes will slow the capital redeployment process down. As a reminder, it is much easier to slow a buy-back than reduce a dividend as the former has a time-band and discretion to implement and the latter generally is a board-level decision.

Secondly, we are aware that discussions around the lack of liquidity in the credit markets are a near daily occurrence these days. The only observation of note is that there is now a new term associated with the market construct – that is, “liquidity cost basis”. In simple terms, due to the lack of market depth and the continued sensational appetite to issue bonds, there is now a higher premium being applied in the market to finding liquidity if you want to own a bond. All we are saying is that the investor concerns over liquidity are not only being priced into the market but those worries have been crystalized with a fancy Wall Street name.

The end result is that investors are demanding a higher premium for the new issues they are taking down, largely due to deteriorating fundamentals in the actual credit.

Now, the second most widely cited explanation for the spread widening is that it is due to the energy sector. If you decompose the spreads it is easier to argue that a notable portion of the weakness is due to the deterioration in the energy sector, whose credit spreads are highly correlated with the lower price of crude oil. However, energy makes up a much smaller portion of the investment grade market (~12%) than it does for the high yield (i.e. ~18%+), which indicates that the breadth of weakness stretches across many other sectors of the investment grade market and is not due to one single risk factor, such as crude oil.

Lastly, we would note that the absolute levels of these spreads referenced on the chart above are also consistent with weakness after the US quantitative easing program was completed and in anticipation of an interest rate hike. We are not sure how much of the spread widening is a result of this less easy monetary policy but the fact is that both QE and the zero interest rate policy forced investors to perpetually search for yield and investment grade credit was a major source of that appetite. To what degree that happened is difficult to handicap but some of those inflows have to reverse given how asymmetric the outcome would be if the Federal Reserve actually embarked on a rate hiking cycle consistent with past cycles, as opposed to a gradual pace of hikes.

Taking a step back, if you look at both the US yield curve and the credit markets, what you find is that both are saying roughly the same thing – that is, there is currently a recession risk embedded in the market, and that there is the potential for the end of this credit and/or economic cycle to be on the horizon.

Take what we have just sketched out any way you want. We are not making a bearish call on risk assets or attempting to sell blood. All we are doing is saying that credit markets, the yield curve and corporate share repurchase trends are signaling some concern sometime over the next 6-9 months. Given that we have not had a recession in 6-7 years, and historically we have had one every four years on average in the modern era, it is not at all unreasonable to start to watch these signals a lot more closely from now on for something more acute.

Above segment from investment newsletter Sight Beyond Sight is re-published with permission from global macro think tank Rareview Macro LLC. Subscription to the daily commentary and trade strategy profiles is available via the firm’s website

Introducing electronic trading to the corporate bond culture is not easy. Fintech initiatives have been trying to crack this egg for 20 years, each promoting the theory that enhanced transparency via electronic trading leads to enhanced corporate bond market liquidity, and ultimately, a robust marketplace for institutional traders to traffic corporate debt and/or via the classic inter-dealer broker business model.

So far, MarketAxxes, which launched in the late ’90s and is best known for bringing small size trades together (under $2mil notional) is one of few that have been able to survive. That said, electronifying the corporate bond market has witnessed several start-up cycles during the past two decades; this current decade counts more than one dozen initiatives; well, that count is “less one” when considering the following news from Finextra.com:

Bondcube, an electronic trading platform for corporate debt, has filed for liquidation just three months after going live.

The startup, backed by Europe’s largest exchange Deutsche Börse, was one of more than 30 new platforms that have emerged in the corporate bond market as a result of new regulations.

Under current capital rules, banks are restricted in the amount of corporate bonds they can hold on their balance sheet, despite the fact that the amount of outstanding corporate debt has risen by nearly 50% to $48 trillion since the financial crisis.

Bondcube and its fellow startups have tried to fill this gap in the bond market by providing buyers and sellers a centralised venue to trade electronically, akin to the various crossing platforms that have emerged in the equities market. The company’s CEO, former Citigroup trader Paul Reynolds, talked of the ambition to make Bondcube, the eBay of the fixed income market.

The problem has been that with so many platforms launching and the existence of longstanding incumbents like MarketAxess, some have struggled to gain the necessary traction.

In a statement, Deutsche Borse conceded that despite succeeding in launching, “sufficient business prospects failed to materialise” and consequently “the shareholders decided not provide further funding”.

Bondcube was formed in 2012 and launched in April this year. It completed its first trade in June, although there were signs that it may struggle for liquidity when a trader at UBS Wealth Management, one of the first participants on the platform, stated that it had taken more than two weeks to find a buyer on Bondcube.

Fintech startup instant message platform Symphony is hearing the sound of trumpets coming from NY Regulators and Bloomberg-challenger backed by consortium of banks now being questioned about deletion and encryption process.

MarketsMuse curators might be a little slow this week in view of following delayed post regarding the roll-out of the instant message chat platform built by a consortium of top banks and intended to displace their dependence on Bloomberg LP…but better late than never…As Symphony Communications Services prepares to launch its much-anticipated messaging service, New York’s financial regulator is raising questions about whether the system can assure that bank communication records will be preserved for overseers. The following is courtesy of American Banker.

NY State Regulator Anthony Albanese

In a letter to Symphony CEO David Gurle (blog post title image), Acting Superintendent of the New York State Department of Financial Services Anthony Albanese asked for further information about Symphony’s document retention capabilities, policies and features.

Noting that “key evidence that regulators used to uncover and investigate” benchmark manipulation schemes has been found in chat rooms, Albanese expressed concern that some banks that are under investigation for rate-rigging are investors in Symphony and have indicated they plan to use it. The letter suggests that before firms begin using a new platform for market related communications, Albanese wants to be sure regulators will still be able to access and audit communications in the event that a firm may be involved in suspicious activity.

The regulator is taking particular interest in “data deletion, end-to-end-encryption, and open source features” of the Symphony platform, the letter said. Albanese said the department would also follow up with banks, requiring them to describe “how they will ensure that messages created using Symphony products will be retained.” The department said it plans to review banks’ responses about their plans to assess whether or not encryption could be used to obstruct regulatory and compliance review, whether firms plan to use deletion capabilities, and whether banks can ensure that employees won’t use open source capabilities “to circumvent compliance controls and regulatory review.”

In an emailed response, Symphony’s Gurley said the platform was designed with compliance in mind, and said the company plans to fully explain Symphony’s technology and its capabilities to regulators.

“Symphony is built on a foundation of security, compliance and privacy features that were built to enable our financial services and enterprise customers to meet their regulatory requirements,” the statement said, according to American Banker. “We look forward to explaining the various aspects of our communications platform to the New York Department of Financial Services.”

Led by Goldman, a group of financial firms invested $66 million in Symphony. The group, in turn, acquired Perzo Inc., a Palo Alto, Calif., company founded in 2012. Goldman, which led the investment among the financial firms, contributed its own internal-messaging developments to the venture.

In addition to Goldman, Bank of America Corp., Bank of New York Mellon Corp., BlackRock Inc., Citadel LLC, Citigroup Inc., Credit Suisse Group AG, Deutsche Bank AG, J.P. Morgan Chase & Co., Jefferies LLC, Maverick Capital Ltd., Morgan Stanley, Nomura Holdings Inc. and Wells Fargo & Co. invested in Symphony.

MarketsMuse Fixed Income Dept. is keeping tabs on industry updates and re-distributes the following news release courtesy of Mischler Financial Group, the financial industry’s leading minority brokerdealer owned and operated by service-disabled veterans.

Stamford, CT—July 22, 2015—Mischler Financial Group, Inc., the financial industry’s oldest and largest minority investment bank and institutional brokerage owned and operated by Service-Disabled Veterans announced that Patrick Beranek, a 20-year industry veteran and most recently the head of Asset-Backed trading for Royal Bank of Scotland (“RBS”) has joined the firm’s capital markets division as Managing Director, Structured Products.

Mr. Beranek previously ran asset-backed trading and syndicate for Mizuho Financial Group Inc. and Bank of America Corp. Prior to those senior sell-side roles, Mr. Beranek was a portfolio manager for Federal National Home Mortgage Corp (FNMA). In this newly-created role at Mischler Financial, Mr. Beranek will oversee primary market activities of structured products. He will report to Robert Karr, Mischler’s Head of Capital Markets.

In connection with the latest expansion, Mr. Karr stated, “The ABS market has undergone a dynamic reset during the past several years, creating new opportunities. Given current economic drivers, a longer-term interest rate outlook and the demand for quality, non-core fixed income instruments, we’re confident that Pat will prove instrumental in the course of elevating Mischler’s role in the primary market for structured products and help bring compelling opportunities to our institutional investor base.”

Added Dean Chamberlain, CEO of Mischler Financial, “We are very pleased to add Pat to our team. Having worked with him before, I know that he has a unique skill-set that will further bolster our structured finance capabilities.”

For the full story, please visit the Mischler Financial Group website via this link

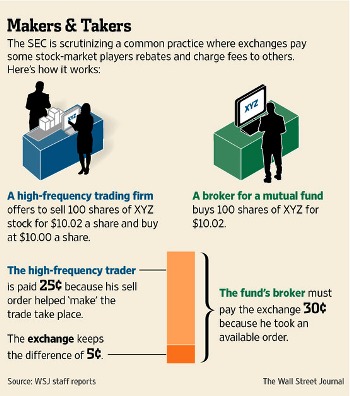

On the heels of the recent NYSE ‘outage’, which actually had little impact on overall equities trading volume, but did lead to volume spikes away from the NYSE and at competing exchanges across the fragmented marketplace, the volume also increased with regard to spirited discussions about market structure. And, whenever talking about market structure, the “rebate debate” insofar as “maker-taker” rebate and fee schemes remain a front burner topic. It is no surprise that many (but not all) sell-side brokerdealers are characteristically in favor of these complex Chinese menus offered by the assortment of major exchange venues and dark pool operators. After all, brokers are ever more dependent on these ‘rebates’ as the race to zero in terms of commission rates paid by institutional customers continues to eat into executing broker income. To counteract the business model impact on BDs, savvy executing brokers have [for a number of years] been making up for lower rates via capturing offsetting revenue from routing customer orders to those bounty-paying trade execution platforms.

On the other hand, nobody should be surprised that an increasing number of institutional investment managers from the buy-side are beginning to “get the joke”, but they aren’t laughing as many realize that brokers are effectively double-dipping by charging their customers a commission and also pocketing kickbacks from competing execution venues that pay those brokers to help light up their screens and provide so-called actionable liquidity execution.

A comprehensive database of global brokerdealers in more than 30 countries, including the US is available at www.brokerdealer.com

To wit, and in our continuing coverage of this topic, MarketsMuse curators spotlighted this week’s story from buy-side publication Pensions & Investment Magazine, which profiles the heightened concern on the part of buysiders and the growing number who are expressing their angst with the SEC, the agency that is ostensibly supposed to ensure fair market practices and protect the interests of public investors. Below are select take-aways from the P&I story.

The Buy-Side Says: “Along with conflict-of-interest issues with rebates, other concerns like increased transaction costs and lack of transparency have added to the complexity of today’s market structure,” says Ryan Larson, RBC Global Asset Management. Added Larson, “Whether it’s SEC mandated, or better yet, driven from market participants themselves, I think it’s time to finally address the elephant in the room and start thinking about possible alternatives to the maker-taker model. … It’s not just the buy side that has been calling for a pilot on maker-taker. It’s the sell side, some of the exchanges, Congress, even members of the (SEC) as well. When you see that diverse of a group calling for change, I think it suggests something very important — whether maker-taker is the right approach. This could be one of the most impactful tests ever taken up in market structure.”

The Not-So-Subjective Market Data Vendor Says: “The whole point of maker-taker is to incentivize display of liquidity in lit markets,” said Henry Yegerman, director of trading analytics and research at financial data provider Markit Group Ltd., New York. “Market participants who place trades that rest passively in a venue, and so add liquidity, get a rebate. Investors who aggressively cross the spread to access that liquidity pay a fee to do so.” Institutional investors that are looking to buy or sell large blocks of stocks “are frequently takers of liquidity,” he said.

The Altruistic Sell-Side Perspective: Joseph Saluzzi, partner, co-founder and co-head of equity trading of Themis Trading LLC, a Chatham Township, N.J.-based agency broker for institutional investors said the link between liquidity and maker-taker doesn’t exist. What maker-taker does increase, Mr. Saluzzi said, is volume. “Liquidity and volume are two different things,” Mr. Saluzzi said. “Maker-taker creates volume, and a lot of that is artificial.”

Mr. Saluzzi said liquidity access is not helped through maker-taker, but by changes in a fragmented market structure that would reduce the number of trading venues. “Liquidity is not helped by rebates, but by less fragmentation,” Mr. Saluzzi said. “Maker-taker is the linchpin of the problems with the market. It’s a relic of a system that was around 15 years ago.”

The Exchange Perspective: Not Everyone Agrees: IEX, the dark-pool operator whose ATS platform is now awaiting SEC approval to operate as a regulated exchange is perhaps the most outspoken critic of maker-taker fee/rebate schemes; customers are charged a flat rate commission irrespective of how an order interacts with prevailing bid-quotes. The New York Stock Exchange came out against maker-taker rebates in testimony by exchange executives in 2014, while Nasdaq Global Markets is running a pricing test program that lowers rebate pricing for select stocks to gauge the effects on liquidity. In two reports this year on the test, Nasdaq has said the lower rebates have had a negative effect on liquidity.

At the other end of the spectrum, executives at BATS Global Markets Inc., which is perhaps the second largest equities exchange as measured by volume, don’t support an outright maker-taker ban and think the rebate paid to liquidity providers matters, “particularly with less liquid securities,” said Eric Swanson, general counsel at BATS, Kansas City, Mo.

[MarketsMuse editor note: Mr. Swanson is a former SEC senior executive who served as Asst. Director of Compliance Inspections and Examinations during the same period of time that his wife Shana Madoff-Swanson, the niece of convicted felon Bernie Madoff, received millions of dollars in compensation while she served as head of compliance for Bernard L. Madoff Investment Securities. According to Wikipedia, Swanson first met Shana Madoff when he was conducting an SEC examination of whether Bernie Madoff was running a Ponzi scheme. Ms. Madoff-Swanson’s father Peter is the brother of Bernie Madoff and is currently serving an extended sentence in a federal jail while Uncle Bernie is serving a 150-year sentence.]

Disruptive Unbundlers, Securities Industry Untouchables, Fintech Aficionados and Innovative Altruists seek to level the investment research playing field, inspiring a bull market for independent research distribution channels, start-ups and disruptive schemes.

Investment research and expert ideas, whether within the context of equities analysis or global macro perspective, has long been the domain of sell-side investment banks, whose research insight is typically bundled as a ‘free product’ within the range of fee-based services provided, including trade execution. Those old enough to remember the ‘dot-com bubble’ days will recall that much of Wall Street’s so-called research was (and arguably still is) notorious for being heavily tilted towards “buy recommendations” in favor of the investment bank’s corporate issuer clients.

This clearly conflicted practice was perfected in the late ‘90s by the likes of poster-boy analyst Henry Blodget (since banned from the securities industry, and ironically, now Editor and CEO of financial media company Business Insider) and was lambasted by securities industry regulators when the “Internet bubble” burst. Those chasing-the-horse-after-the-barn-door-closed efforts since led to a regime of regulation and firewalls intended to distance in-house research analysts from their investment banker brethren so as to mitigate biased recommendations and conflicts of interest. Compliance officers across the industry found themselves facing a host of new rules, and that ‘compliance contagion’ served as the catalyst for a spurt in “independent research boutiques” offering “unbundled” and un-conflicted research sold as a stand-alone product with no ties to execution or trading commissions.

However compelling the notion, and despite the regulatory impetus to foster the growth of independent research boutiques, the business model for these firms has proven challenging during the past 10-15 years. Many boutique research firms floundered or failed for several crucial reasons, including but not limited to (i) the burdensome costs and means associated with creating a stand-alone brand, (ii) the challenge of delivering consistent and compelling content to institutional investment managers and sophisticated investors at a price point that could prove profitable and (iii) the non-trivial logistics required to deliver content in a compliant manner. In the interim, regulators stood by and observed, and digital delivery mechanisms for independent researchers only slowly evolved. Investment banks, never shy when it comes to creative workarounds, bolstered their research ranks and produced more content, even if mostly undifferentiated, but still promoted by the strength of the investment bank’s brand.

All of this is about to change again, causing some to conclude that regulatory market moves in cycles every decade or so, much like the stock market moves in cycles. The current bull market case for unbundled independent research is not a result of efforts by get-tough-on-Wall Street types such as New York Attorney General Eric Schneiderman or Massachusetts’ kindred spirits Elizabeth Warren and William Galvin, and the bull case is certainly not because of any efforts made by the SEC. To a certain extent, the positive outlook for those in the unbundling space is based on Moore’s Law and the advancement of Fintech-friendly applications, but it is more directly attributed to a new European Union law inspired by MiFID II, that if passed as expected, will require investment managers to pay specifically for any analyst research or related services they receive. With that new rule (which includes more than a few line items), many large money managers are starting to follow the proposed rules globally; investment banks in the U.S. (and obviously those in Europe) are devising new business models for one of their oldest and highest-profile functions: offering ideas to customers that banks can monetize through commission-based services.

More than some across the major continents believe that however much top investment bank brands are a decidedly powerful selling tool for research product, the power of the internet has enabled the distribution of independent research and enables a Chinese menu of pricing schemes via a continuously-growing universe of independent portals that invite content publishers to sell their products using an assortment of social media-powered distribution channels and revenue-sharing schemes.

Bloomberg LP has created its own independent research module accessible by 300,000+ subscribers in direct competition with Markit, the financial information services provider. Earlier this year, Interactive Brokers (NASDAQ:IBKR), the web-powered global online brokerage platform that provides direct market access to multiple exchanges and trading venues across the entire asset class spectrum quietly began enhancing its offering of third-party professional and institutional-grade research. IB’s 300,000+ accounts comprising professional traders and institutional clients may subscribe to research made available in the trading platform, Trader Workstation (TWS). At the same time, IB began promoting these third-party research providers via IB Traders’ Insight, a blog embedded within the firm’s Education module that covers the full range of investment styles from more than two dozen content providers.

While bolstering objective research content is a natural business extension for those having captive brokerage clients and for terminal-farm behemoths, perhaps even more interesting is that start-ups in the unbundling space are starting to percolate.

On the European side of the pond, UK-based SubstantiveResearch, created earlier this year by former EuroMoney Magazine publisher Mike Carrodus, is positioned to be an institutional research thought- leader that curates and filters both independent and sell side global macro research, with a sleeve that hosts regulatory events for investment manager content consumers and sell-side content providers. Start-ups in the US include among others, Airex Inc. , which dubs itself “the Amazon.com for financial digital content” and recently secured funding from fintech-focused merchant bank SenaHill Partners. TalkMarkets.com is another notable entrant to the space, and was created in late 2014 by Boaz Berkowitz, a former “Bloombergite” who was also the original brain behind Seeking Alpha. From the traditional financial media publishing world, industry stalwart Futures Magazine, recently re-branded as “Modern Trader” and the parent to hedge fund news outlet FinAlternatives is also embracing the research content unbundling movement as a means towards capturing more Alpha and better monetizing relationships with content providers. Each have their own business models, including the use of cloud-based technology and coupled with the muscle of creative online marketing, social media tactics and search-engine ranking techniques.

While the start-up space is often littered with short shelf-life stories, these new unbundled research distribution vehicles are being enabled by the fintech revolution and embraced by distributors of content, high-profile independent research providers, as well as by at least one major bank seeking to hedge its internal bets; earlier this year, Deutsche Bank inked a deal with upstart Airex, such that DB’s proprietary equity research is available on a delayed basis and can be purchased by any AIREX Market shopper. In the case of now 6-month old TalkMarkets, they are embracing an advertising-based business model, which is predicated on building an outsized audience of sophisticated retail investors for prospective advertisers. To date, they have enlisted more than 350 content providers and 10,000+ registered users. While there is no cost to access the platform, content providers are able to upsell subscription-based services and at the same time, earn ‘points’ that can be converted into the private company’s equity shares.

Neil Azous, Rareview Macro

According to former sell-side global macro strategist Neil Azous, the Founder/Managing Member of think tank Rareview Macro LLC, and the publisher of subscription-based “Sight Beyond Sight” which is now being distributed across several channels apart from the firm’s website (including via Interactive Brokers), “Truly superior, high-quality content, including actionable ideas remains relatively scarce, but the fact remains, content has become commoditized. The good news is that banks are not the sole source of carefully-conceived research and the better news is that conflict-free content publishers can now more easily distribute via a broad universe of narrow-casting, web-based channels.”

Added Azous, “For independent research providers and trade idea generators, it’s arguably a watershed moment. As new rules take shape, content publishers, including those who previously worked under investment bank banners, can now reach an exponentially larger universe of content buyers through these new distribution channels. It’s a numbers game; instead of working inside an investment bank and trying to ‘sell’ a traditionally high-priced product to a relatively narrow list of captive clients, the more progressive idea generators can re-tool their pricing and make their product available to exponentially more buyers, and in a way that conforms to and stays within goal posts of compliance-sensitive folks.”

However much it makes sense to foster the easy distribution of independent and un-conflicted research, Wall Street et. al. is not going to easily abrogate their role for providing ideas or forgo the trade execution commissions derived from those proprietary ideas. Banks are reported to be devising new pricing models for investment research in view of EU proposals that could prevent research from being paid for using dealing commissions. In an unbundled world, where payments are separated, competition for equity and credit research may increase as asset managers look beyond traditional sources, which may trigger fragmentation. They may also move research in-house. The U.K.’s FCA, which is driving the debate, has endorsed the EU proposals.

As noted within the most recent edition of Pensions & Investments Magazine, Barclays PLC, Citigroup Inc., Credit Suisse Group AG and Deutsche Bank AG are working with clients to come up with pricing for the analyst research customers receive, according to bank executives. Prices are expected to range from roughly $50,000 a year to receive standard research notes, up to millions of dollars for bespoke research and open-door access to analysts.

“We are working to change the mind-set so that fund managers understand that research should be treated as a scarce resource. There is a great opportunity to tap into experts in their fields at brokers, but we need to really think about the value of research and determine the right amount to pay for it,” said Nick Anderson, head of equities research at Henderson Global Investors.

The following [excerpted] analysis is by Bloomberg Intelligence analysts Sarah Jane Mahmud and Alison Williams and helps summarize the current outlook. It originally appeared on the Bloomberg Professional service. Continue reading →

How big are ETFs these days? Even Kevin O’Leary, aka “Mr. Wonderful” of ABC’s “Shark Tank” is getting into the game. On Tuesday, O’Leary was on the NYSE floor to launch the O’Shares FTSE US Quality Dividend ETF, (ARCA NYSE:OUSA): a basket of high-dividend stocks.

But he’s not doing this just to enter the crowded ETF space, which already has 1,700 ETFs and more than 50 ETF providers.

As noted by the coverage from CNBC, “Mr. Wonderful” is entering the exchange-traded fund world as an Issuer because he needed an investment vehicle for the equity portion of his family trust, which he started in 1997. O’Leary claims he wanted an investment vehicle that was rule-based, first and foremost, so no one would tinker with it.

And he wanted dividends. Why dividends? As O’Leary accurately opines, 70 percent of the returns in the stock market over the past decade or so have come from dividends.

But O’Leary did not just want to buy a basket of the highest-yielding ETFs. You can get that already with Vanguard High Dividend Yield, and you can get variations, like the iShares Select Dividend, that screen by dividend-per-share growth rate, or the Vanguard Dividend Appreciation ETF, which focuses on companies that have steadily increased dividends. O’Leary’s rule-based system is predicated on the following:

A total yield close to 3 percent

with 20 percent less volatility than the market

with stocks that all had strong balance sheets

OUSA is therefore comprised of 140 stocks selected from the FTSE USA Index, comprised of 600 of the largest U.S. publicly-listed equities.

Given the high-profile presence and PR power of O’Leary, O’Shares made its debut on Tuesday in heavy volume. It’s the latest in a flurry of new ETF launches this month; now with 28 new funds, July is already tied for the most ETF launches of any month this year.

Marketsmuse updates that fund giant John Hancock Investments will partner with Dimensional Fund Advisors on six “smart-beta” exchange-traded funds, according to paperwork filed with regulators early on Monday.

Dimensional, based in Austin, Texas, is one of the earliest proponents of factor investing. They blend elements of index-based investing and active investing in order to predictably exploit market returns and minimize trading costs. Many of today’s smart beta products — from index providers including FTSE Russell, WisdomTree, Research Affiliates — are based on a similar premise.

John Hancock unveiled in its preliminary prospectuses for the factor-based ETFs that DFA, the market-beating investment firm that adheres to the academic work of Eugene Fama and Kenneth French, will be the sub-advisor for its ETFs. John Hancock has worked with DFA on mutual funds and asset-allocation strategies since 2006.

John Hancock initially filed plans for ETFs nearly four years ago, but has yet to bring an ETF to market. However, a new filing with the Securities and Exchange Commission indicates the firm is getting closer to launching its first ETFs.

The new filing provides details and expense ratios on the proposed ETFs. For example, the John Hancock Multifactor ETF, which is expected to charge 0.35% per year, will track an index comprised a subset of securities in the U.S. Universe issued by companies whose market capitalizations are larger than that of the 801st largest U.S. company at the time of reconstitution. In selecting and weighting securities in the Index, the Index Service Provider uses a rules-based process that incorporates sources of expected returns. This rules-based approach to index investing may sometimes be referred to as multifactor investing, factor-based investing, strategic beta, or smart beta.

John Hancock manages nearly $130 billion in mutual funds and money-market funds. Dimensional manages $406 billion. Dimensional already advises on John Hancock-branded mutual funds that have $3.2 billion in assets.

Now that InteractiveBrokers is turning up the heat and joining the “unbundling movement” by offering independent research via its world-class trading platform, MarketsMuse editors spotlighted the following comments courtesy of global macro sage Neil Azous, Founder/Managing Member of Rareview Macro LLC from today’s IB feed..If you’re a hedge fund-type, you will either smile, smirk or throw a rock at your computer..

Neil Azous, Rareview Macro

A few of our hedge fund buddies have asked us to bring back “the old-school Neil” and tell you what I think will happen in the next 48-hours. We aim to please, at least sometimes, so therefore today’s note has a lot of “hedge fund speak” and is very short-term in nature. Here we go.

If you ban selling, threaten to arrest short sellers and suspend over half the market, then at some point Chinese equities will inevitably close positive. Add in some good old fashioned government buying of what actually remains open and it is no great surprise that equity markets closed positive in China.

Of the 2,754 shares traded in Shanghai, 1,700 were suspended but the ones that were opened had virtually a 100% up-day. All 194 of the 484 shares that are still open for trade on the ChiNext Board – the poster child for speculation – rose limit up 10%. The three main index futures – CSI 300 and CES China 120 – closed limit up 10% and FTSE China A50 futures closed up +17%. The 5.8% gain in the Shanghai Composite was the largest since 2009.

While the invisible hand of China’s government has set a positive bid-tone for the rest of global risk assets today, it also increased the probability of further PnL duress for long/short hedge funds here in the old US of A.

Sadly, the desire by the long/short hedge fund strategy to reduce overall gross exposure over the last week has been very low.

The fact is that the majority believe that the earnings bar going into this reporting season is so low that you can crawl over it on your knees, and that the dispersion of opportunities remains high due to M&A activity or event-driven catalysts. The last thing this investor base wants to do is lose core positions on account of Greece or China. In Greece, the opportunity cost has been high over the years, and in China’s case, since none of them have really any meaningful direct exposure, the mindset is that the spillover effect to US equities is marginal at best.

As a result, long/short hedge funds remain long on single stocks, and to at least show some appearance to their investors that they are being prudent given the top-down concerns globally they have OVER-purchased a lot of market-related protection, or have used blunt instruments to get really short of the market outright. Put another way, their gross exposure is roughly the same as where it was last month, before the very recent global margin call kicked in, but there is large contingency now running TOO NET SHORT.

To continue to dazzle you with words like “code-red”, it does not take a genius in this business to look at all the usual short-term hedge fund indicators and recognize that many of them are at extremes – that is, put/call option ratios are at 18-month highs, prime brokerage position reports show the net short position at multiple standard deviations above the average over the past year, etc.

So what does the fact that long/short hedge funds are extremely long single stocks and over-hedged actually mean? Continue reading →

MarketsMuse is keeping its fingers on the pulse of the FinTech movement, and aside from the initiatives that we’ve spot-lighted taking place courtesy of Wall Street Wonks, its more than fair to say that London is fast becoming the hub of innovation and technology, and attempting to lay claim to the position as the fintech capital of the world, strengthening its place within the global financial market.

To put this into perspective, the UK is now the fastest growing region for fintech investment with deal volumes growing at 74% per year since 2008, topping $265 million in 2013 alone (Accenture). That’s twice as fast as its American counterpart Silicon Valley.

Commonly referred to as Tech City, London’s fintech cluster is now thriving, nurturing entrepreneurs, new business models and technologies. Last year alone, over 15,000 (UHV Hacker Young) new businesses were set up in EC1V, more than any other area in the UK. These are being celebrated and promoted with the help of new London initiatives such as the Fintech 50 and the first official Fintech Week.

Here are 3 of the top 7 tech start-ups that have added some air to the latest “tech bubble.”

Osper has come up with an innovative way to create a banking service than can be used by children, combining prepaid debit cards and smartphone apps controlled by both them and their parents. The approach could potentially reach a market underserved by most banks, but which may also be embraced by parents keen to educate their children early on about how to manage money.

Coinfloor is a new VC-backed Bitcoin exchange that prides itself on complying to strict anti-money laundering and “know your customer” procedures, despite the fact that Bitcoin isn’t classified as money by the UK’s Financial Conduct Authority.

MarketsMuse senior editors have quickly canvassed a broad assortment of “market structure experts” and industry talking heads who have been at the forefront of debating the pros and cons of market electronification, multiple market centers and the underlying issue: “Is Market Fragmentation Good, Bad or Ugly?”

For those who might have just landed on Planet Earth, the debate (which is ongoing via industry outlets such as TabbForum, MarketsMedia, and most others) boils down to whether multiple, competing electronic exchange systems enhance overall market liquidity and make it ‘easier and better’ for institutions and retail investors to execute ‘anywhere/anytime’ via the now nearly two dozen “ECNs”, “Dark Pools” that offer a Chinese menu of rebates, kickbacks and assorted maker-taker fee schemes (e.g. ARCA, BATS etc), or whether someone should try to shove the Genie back into the bottle and revert to the days of yore when the NYSE was the dominant listing and trading center for top company shares, and complemented by a select, handful of regional stock exchanges, most notably, The MidWest Stock Exchange, The American Stock Exchange, The Philadelphia Stock and the Cincinnati Stock Exchange.

Despite the fact that CNBC talking heads dedicated the entire day’s coverage to the NYSE snafu with rampant speculation as to whether the day’s outage was due to a cyber attack by the Chinese in their effort to distract the world from the dramatic drop in China-listed shares, whether it was a Russia-based malware attack, or perhaps even an ISIS-born cyber-terrorist attack that also impacted United Airlines)–the fact of the matter (one that CNBC seemed oblivious to) is that those who wanted to execute stock trades through their brokers were able to do so without disruption, simply because those brokers routed orders to a drop down menu of exchanges that compete with the NYSE..

Yes, the NYSE lost a day’s worth of fees attached to every order they typically execute on a normal day (not a good day for exchange President Tom Farley)–but more than half of the market structure experts who have continued to campaign against market fragmentation have [temporarily] flip-flopped today and have acknowledged that were it not for multiple competing exchanges, today would have been a real headache for US stock market investors and brokers. No doubt CNBC and others who were fixated on this outage will be able to turn their attention back to what is taking place in Greece, China and other topics that actually do impact the price of global equities.

Do you hear that? That stampeding sound you hear is coming from fund managers scurrying to get into the currency-hedging trade.

Currency hedging ETFs have been in vogue this year given the ultra-lose monetary policy across the globe and a strong U.S. dollar against a basket of other currencies. The bullish trend in the dollar is likely to continue as the Fed is primed to increase interest rates for the first time since 2006 later this year, as the U.S. economy roars back to life.

While cheap money flows are making international investment a compelling opportunity for U.S. investors this year, a strong dollar could wipe out the gains when repatriated in U.S. dollar terms, pushing international investment into the red in spite of well performing stocks. As a result, investors are flocking to currency hedged ETFs. This has a double benefit. While these ETFs tap bullish international fundamentals, they dodge the effect of a strong greenback.

As is often the case on Wall Street, the natural worry is whether the rush might come too late. Foreign exchange dynamics present earlier this year have abated somewhat, making the need to protect against currency movements less urgent for the moment.

With the race to the bottom heating up among global central banks, it’s no wonder fund managers are looking to capitalize.

MarketsMuse special update-courtesy of MarketsMedia reporting with a refreshing reprieve from all-things Greece …While Silicon Valley salivates over the next social media-powered “Unicorn”, the global financial industry is fixated on FinTech. Just like the litany of aspiring app companies accelerating the ‘next great idea’ produced by West Coast Wonks, as noted in today’s coverage by the Wall Street-focused, tech-centric media platform, MarketsMedia.com, financial-technology startups need capital to turn their idea into a viable business, and more important in most cases, they need the right strategic advice to operate, expand and then potentially merge or sell the enterprise.

Venture capitalists and angel investors can provide initial funding; consultants can help with operations; investment banks can arrange additional capital raises and advise on M&A. SenaHill Partners is unique in that it has stitched together all that is needed over the ‘fintech’ lifecycle.

“Our merchant-banking value proposition connects the dots at every strategic level between global financial institutions and the entrepreneurial innovators of financial technology,” SenaHill Managing Partner and Co-Founder Justin Brownhill told Markets Media in a June 29 telephone interview. “We feel that we can get the right ideas in front of the right people better than anyone else. That’s the mission of our organization.”

Neil DeSena, Senahill Partners

As profiled by MarketsMedia.com, New York-based SenaHill, founded in 2013 by Wall Street veterans Neil DeSena and Brownhill, offers principal investing via its SenaHill Investment Group, LLC unit, and investment banking through SenaHill Advisors, LLC.

Wall Street is a relationship-driven business, a fact that is not lost on SenaHill. The company splits its formidable roster of talent into two categories: active advisors, formerly top people in the financial industry who can help startup and emerging fintech companies get the right exposure and introductions; and inactive advisors, who provide guidance, insight and background from their current positions in the industry.

SenaHill’s advisors include Stanley Young, formerly the chief executive officer of NYSE Technologies; David Ogg, CEO and founder of Ogg Trading; Joseph Wald, CEO of Clearpool Group; Sam Ruiz, an independent advisor and former head of equities trading at Nomura; and Craig Marshall, a start-up vet who is credited with creating the general-purpose prepaid category.

“As companies come to us, we can reach back out into the industry to these senior resources in our network and ask them about the space, the people, the product and more,” said DeSena, who headed REDI in 2000-2006, when the global multi-asset trading system was owned by Goldman Sachs.

For the full story from MarketsMedia.com, please click here

First Trust Advisors L.P. expects to launch a new etf, the First Trust NASDAQ CEA Cybersecurity. The fund seeks investment results that correspond generally to the price and yield (before the fund’s fees and expenses) of an equity index called the Nasdaq CEA Cybersecurity IndexSM.

Cybersecurity is gaining global attention following recent high profile security breaches. With the heightened need for cybersecurity solutions, First Trust believes this could be a favorable time to invest in cybersecurity companies. The index is designed to track the performance of companies engaged in the cybersecurity segment of the technology and industrials sectors. It includes companies primarily involved in the building, implementation, and management of security protocols applied to private and public networks, computers, and mobile devices in order to provide protection of the integrity of data and network operations.

This new ETF includes companies primarily involved in the building, implementation and management of security protocols applied to private and public networks, computers and mobile devices in order to provide protection of the integrity of data and network operations.

As more companies are experiencing high-profile cybersecurity breaches, the industry is gaining global attention. With the heightened need for cybersecurity solutions, First Trust believes this could be a favorable time to invest in cybersecurity companies. The index is designed to track the performance of companies engaged in the cybersecurity segment of the technology and industrials sectors.

Hull Tactical Asset Allocation, LLC (“HTAA”), announces the launch of the Hull Tactical US ETF (“HTUS”), an actively managed exchange traded fund designed by industry veteran Blair Hull. The ETF is designed to deliver hedge fund-type management and trading tactics to a broad investor audience.

Working in partnership with Exchange Traded Concepts, LLC, the white-label ETF issuer platform, the team at HTAA believes that the Hull Tactical US ETF will be attractive as the market for institutional-quality equity products continues to grow.

HTUS is constructed to perform under all market conditions, with an investment objective of long-term capital appreciation, guided by the firm’s proprietary, patent-pending, quantitative trading model. The model selects indicators that HTAA believes can best forecast the next six months of return of the S&P 500. It takes long or short positions in ETFs, leveraged ETFs or other securities that seek to track the performance of the S&P 500 based on the model with the remaining assets in the portfolio being held in cash.

The fund is a good option for investors seeking to stay invested in the market under all conditions. “A wide range of investors – from sophisticated retail investors, to independent advisors to endowments and pension funds in the institutional space – should find our product advantageous,” says Steve McCarten, Chief Operating Officer of Hull Tactical Asset Allocation.

Given the current equity market condition, investors can expect to reduce volatility exposure to the equity market through this fund. This is especially true as the long-short positions taken by the fund help to withstand volatility. Moreover, the fund is expected to provide higher diversification benefits as the long strategy is believed to be highly uncorrelated to the traditional asset classes.

Pot has been generating lots of buzz both in the public and private sectors.

Twenty-three states and the District of Columbia have legalized marijuana, either for medicinal or personal use, while an additional 13 have planned votes by 2016. If the trend toward legalization continues, there’s big profit potential, considering $2.5 billion in legal sales last year—and the estimated $60 billion in illegal sales.

There is an ETF for just about any investing theme you can think of. Still, marijuana is a relatively new legal industry regionally, with very few legitimate public companies in the sector that have generated revenues and that have been run by officers who know what it takes to be a public company.

Companies that would be included in any serious ETF would likely be limited to legitimate reporting companies. Some of these companies included in an ETF would almost certainly be companies that service the marijuana industry but that are much larger and focus on farming and cultivating throughout the broader agricultural sector.

One ETF inclusion would be a so-called hemp-friendly bank, which is yet to be determined. Federal laws and regulations still make the business of marijuana almost impossible to bank on. It is currently a high-cash business. You know that one bank will be the first to embrace the industry, and marijuana entrepreneurs and store owners almost certainly will flock to that bank. Again, this bank is a draft to be announced at a later date

However, if we look on the other hand, pot may be a perfect example of when an exchange-traded note (ETN) makes more sense than an ETF. ETNs don’t have to hold any of the stocks. The notes are unsecured debt obligations that are basically, promises to pay the returns of an index. So it doesn’t matter if the stocks are illiquid or not. What matters most is the creditworthiness of the ETN issuer.

ETNs were first introduced 10 years ago for this very purpose—to get into places that were particularly tough for ETFs to track. For example, the iPath India ETN (INP) was launched in 2006 to get around the strict foreign ownership restrictions that made an ETF impossible. It accumulated more than $1 billion within two years.

An ETN issuer could do the same thing, using a self-made pot index or something like the MJIC Marijuana Global Composite Index. The downside to ETNs is there is always risk that the issuer will default, just as with a bond. For investors “jonesing” hard enough for a pot ETF, this may not matter.