Jane Street Capital, the quant-centric proprietary trading firm best known for its dominant role in the ETF marketplace–including its role as a liquidity provider for stocks and options as well as exchange-traded funds to buy-side accounts– has a new arrow in its quiver; making markets in corporate bonds. The firm disclosed that it is lifted its anonymous veil and is now a ‘disclosed dealer’ on electronic bond trading platform MarketAxess (NASDAQ: MKTX).

Shall we guess whether the 6-pack banks and their first cousins–the industry’s legacy source of liquidity to buy-side managers navigating the corporate bond market landscape are (i) happy to have a new competitor, (ii) happy not to have to make markets and tie up balance sheets with inventory of hard-to-move corporate bonds or (iii) f–king pissed that tech-focused prop trading firms are now invading a secondary market product area that banks have viewed as their exclusive territory since time began?

As noted by WSJ reporter, Matt Wirz, investment banks and brokerages are the main go-betweens for money managers looking to buy and sell corporate bonds, about $25 billion of which trade daily in the U.S. Now, Jane Street Capital LLC, has begun offering the same service to investment firms on electronic trading platform MarketAxess and has recruited about 60 clients, people familiar with the matter said.

The move puts Jane Street in direct competition with traditional dealers like Goldman Sachs Group Inc. and JPMorgan Chase & Co. It also shows how bond markets are being transformed by electronic and algorithmic trading, innovations that swept stock and currency markets more than a decade ago.

Jane Street’s headquarters are a five-minute walk from Wall Street, but in some ways the firm is more akin to a Silicon Valley startup than an investment bank. “They have a different approach—there’s not a lot of sales and a lot of technology,” says Mike Nappi, a bond trader for mutual-fund manager Eaton VanceCorp. who has bought and sold bonds through Jane Street. “That’s different from a traditional bank where they have a lot of sales and the technology is more like Microsoft Excel.”

By joining those ranks, Jane Street aims to get recognition from asset managers for the balance sheet it uses to buy and sell with them, ultimately boosting the amount they trade with the firm, said Matt Berger, the firm’s head of fixed income and commodities trading. Jane Street trades about $550 million worth of corporate bonds in the U.S. every day, he said. This amounts to about 2% of the overall market, five times more than the firm traded two years ago.

That expansion would have been impossible without the recent spread of electronic bond trading.

Technology-driven trading firms like Jane Street and Virtu Financial LLC emerged after stock exchanges electronified in the 1990s, connecting buyers and sellers through computers and reducing trading times to fractions of a second. The firms’ computer scientists built programs to cull market data and identify profitable trades that humans missed. Now, quantitative trading firms dominate the stock market.

Electronic trading has been slower to catch on in debt markets because bonds typically trade over-the-counter rather than on centralized exchanges. That has begun to change over the past five years as banks and money managers turn to electronic trading and data analysis to trim costs and to connect to more trading partners. Electronic trading platforms like MarketAxess have given Jane Street and other quantitative investors venues to apply the technology they used in other markets.

MarketAxess accounted for about 18% of all U.S. investment-grade bond trading last year, up from 12% in 2014, according to data from the company.

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editorvia cmo@marketsmuse.com

Jane Street, founded by four partners including Michael Jenkins and Robert Granieri, now has about 50 bond salespeople and traders. Recruiting materials tout chess facilities, office gyms, math puzzle contests.

The firm trades less debt overall than most banks, which still employ hundreds of human sales and trading staff. But when it comes to its inventory of corporate bonds, “we are on par with the banks,” Mr. Berger said.

Jane Street hold bonds on its balance sheet for days or weeks to facilitate so-called portfolio trades of bundles of bonds often tied to ETFs. The portfolio deals normally range from $50 million to $750 million but can go as high as $2 billion, a person familiar with its trades said.

Stock Price Implosion Leads Some to Challenge Current Market Structure; HFT Firms Are Under Attack, Again…

Heads Up to High-Frequency Firms: Time to Hire a PR Crisis Manager Again, Call Your Lobbyists, Book Your Plane Tickets to Washington DC.

Before “bidding on” to the anti-HFT and anti-ETF remarks circulated by the assortment of market pundits appearing on Bloomberg, Reuters or the financial media megaphone channel, CNBC, you should know that SecTres Mnunchin has already weighed in. So has the SEC’s favorite tech entrepreneur, Mark Cuban. So has icon stock investor Leon Cooperman, who has the ear of Mnuchin and others. There’s a whole ‘hang-em-high’ crowd assembling to lay blame on high-frequency trading for the latest market routs. According to CNBC, Trump favorite Mike Flynn was overheard shouting to Mnuchin and Trump: “Lock them up!”

NYSE DMM Citadel Securities started as a HFT prop trading firm

But, unless you’ve been investing in or trading in the equities markets for at least 20 years, you probably have no conception of a simple premise: markets go up and markets go down. Blame games are easy to play, equities investing is not always easy.

Traditional drivers to stock price movements include simple, time-tested fundamentals: the interest rate environment, the economic cycle, the value of the US dollar vs. other currencies, corporate revenue and profit, corporate debt levels, consumer debt levels, trends in residential real estate prices and other consumer optimism metrics. Yes, you can throw in the degree of confidence in the current government administration and a bunch of other geopolitical stuff (including tariff wars, Brexit event, and total uncertainty in many countries’ leadership–including the US) into the mix. We’ve all grown accustomed to the minute-to-minute chaos caused by the current president. His impact on stock prices is powered by his Twitter comments about China, the Federal Reserve Chairman, and blaming the latest government shutdown on democrats. Beyond that, institutional investors can only make investment decisions based on reality within context of company earnings reports and not easily-fudged economic data. Investors should NOT make decisions based on a reality TV show produced in Foggy Bottom.

But, we should agree on one thing: the combination of complacent investing, a belief that prices of company shares will go up year after year is a fool’s view. The topic of debate in this post is whether the evolution of high-frequency trading (aka HFT) weaponry has contributed (yet again) to the large (downward) percentage moves in stock prices during the recent weeks. The sell-off, which arguably began during the first week of October, has led to an approximate 20% decline in the leading stock indices from the record highs. Many individual share prices have suffered bigger mark-downs, most notably tech sector stocks. Before asserting that high-frequency trading algorithms are the culprit, one need to ponder whether those same HFT tools also contributed to the nearly 50% gains the stock market has enjoyed since the 2016 US presidential election (two years ago)?

Whatever black swans have been flying over head for the past 6 months, now that equity prices have suffered multiple-day declines of 1%-3% (and the interim 1%-2% “dead cat bounce”) we need to blame someone!! After all, our very own president has been unwavering in his leadership mantra: “When the shit hits the fan, blame someone else for the problem!”

Let’s say you want to blame HFT firms for the slide. Considering the fact that today, the 3 largest NYSE market-makers are better known

Specialist traders work at a Virtu Financial booth on the floor of the New York Stock Exchange April 16, 2015. Shares of electronic trading firm Virtu Financial Inc rose as much as 24.6 percent during their IPO, valuing the company at about $3.23 billion. REUTERS/Brendan McDermid – RTR4XMJS

for their legacy as high-frequency trading outfits, its easy to be cynical. These are ‘not your father’s NYSE specialist firm’, these are young quant jocks who made a ton of money as HFT prop trading shops starting back in the early 2000’s, and more recently, used some of that cash to purchase the legacy NYSE market-maker firms; the firms responsible for maintaining fair and orderly markets in NYSE listed companies. Now known as NYSE “DMMs”, they (actually their computers) also have the “first look” at orders to trade shares in which they are now the designated market-maker for. Instead of old-fashioned auction markets, these folks utilize algorithmic trading tools to match buyers and sellers and also trade for themselves. As a consequence, there is circumstantial evidence these firms are, to some extent, culpable for the rapid reflex moves in share prices.

Keep in mind, the flip-side is that these ‘HFT black boxes’ are also providing instantaneous liquidity, price transparency, and facilitate exiting or entering a investment position in less time than it takes to hit a ‘send’ button (until someone unplugs the machine after realizing they’ve risked the entire firm’s capital). Further, because everything happens in nano-seconds, one can argue that bear market cycles –periods that typically reflect recessionary pressures and in turn, signals that lead to a negative impact on the value of a company’s equity shares—are now much shorter in duration when compared to cycles going back 60-70 years.

To the first question, who can forget the May 2010 ‘Flash Crash’—an event that was certainly connected to HFT computers plugged into the walls surrounding the NYSE and NASDAQ computer server farms–and then became unplugged by humans when markets cratered due to a “fat finger” episode. We’ll tell you who cannot remember that event (other than having read about it years later): upwards of 1/3 of current ‘senior’ Wall Street quant jock HFT programmers who code the HFT machinery. Many of them were mining bitcoins in their MIT dorm rooms back in 2010. How many of the current generation of ‘systematic traders’ who now oversee billions of dollars were beyond high school in 2004? How many current trading desk wonks were around during the dot com bubble? How many folks who worked on trading desks in 1987 are even still alive, no less working in the business? Have you gotten the point, yet?

Because our pundits have accurately predicted this latest market down draft, allow us to further predict that we want to be “long on” private jet services to Washington (NYSE: BRK.A) and we’d love to invest in engagement contracts issued by PR Crisis Management gurus who represent these folks; they are presumably getting calls already by the best-known HFT honchos, starting yesterday.

Let’s be clear, the fundamental economic underpinnings that power equity prices have been sending mixed (warning) signals for months. OK, employment figures have been good, but Trump told us while campaigning for president that “US Employment figures are fake and fraudulent.” Yes, corporate earnings have met expectations, but nobody has delivered out-sized reports, and many companies have been sweating to provide realistic expectations, not wild-ass projections. According to recent polls, nearly 50% of Fortune CFOs are anticipating a recession will hit the US economy in 2019. 80% of CFOs believe a recession will be upon us before the end of 2020. Many multi-nationals based in the US are lamenting “Tariff Man” tweets. He says ‘US companies with US employees that make/sell products to US consumers will benefit, and the big companies have plenty of money to cushion the blows..” Really?!

So, fundamentals have been weakening during the past 2 quarters (unemployment figures aside). Even for those who subscribe to technical analysis and historic charts, the writing has been on the wall for months: “Caution Mr. Robinson, Caution!”

High-flying tech company shares started cracking in the 2nd quarter of 2018. They’ve been under an assortment of pressures that range from severe government and shareholder scrutiny to simple supply/demand obstacles impacting their business models (e.g. FB down nearly 40%, GOOG down 30% from its high, AAPL down 40%, AMZN down etc etc.) Bank stocks have been pummeled for the most part, even if GS’s latest beating is connected to yet another multi-billion dollar scandal. Big ticket corporate acquisitions made in the past 2 years have resulted in transition management problems. Corporate balance sheets have become increasingly overly-bloated with debt, thanks to folks on Wall Street who came up with a new pitch to corporate treasurers starting back in 2011: “We’ll float your bond offering (and get a big fee), you use the proceeds to repurchase outstanding shares, and you’ll make your EPS numbers look fantastic; everyone wins!!” Until the music stops, of course. Corporate share repurchases have been credited with keeping equity prices stable and moving higher for upwards of seven years; the brokers are making nice commission on executing those buybacks and all is good with the world, until its not.

Stock market chartists started raising red flags in October. Corporate debt issuance came to a crashing stop in the last 6-8 weeks. That was a big signal. Less than two dozen Fortune companies have actually been buying back debt in the past quarter in preparation for the next shoe to drop; the one with the word ‘recession’ stamped on the bottom of each shoe. The notion that corporations should unwind the ‘sell debt, buy shares’ trade –by issuing new shares and using the proceeds to balance the balance sheet and repurchase outstanding debt is an idea that no investment bank would even suggest in his sleep, no less in an office. It would be professional suicide for a corporate CFO to even suggest that idea makes sense. Geopolitical impact re Trump’s tariff war is hitting US companies and US workers, even if not the Trump Hotel enterprise. The corporate tax cut was a short shot of heroin that stimulated the stock market, but increased the Federal deficit by nearly $1trillion. (Let’s not forget that Trump campaigned on reducing debt, not increasing it–but so does every other candidate). Now people are coming off the sugar high and that’s how/why stock prices revert to the mean.

Tariff Wars, Brexit and the assortment of geopolitical catastrophes have all been thrown into the mixing bowl. Crude oil prices have been crushed–along with the share prices of companies that drill, process and sell oil-based products. Yes, we’ll repeat: employment figures have been great, but as Donald Trump said throughout his presidential campaign, “Nobody can believe government employment figures, they’re all fake news!”

When weighing the assortment of fundamental signals that have been brightly broadcast throughout the past 9-12 months—and certainly since October of this year, anyone who had not re-balanced or pared down exposure to equities has no business investing in stocks. Its easy to say “Ok, 20-20 hindsight is great..blah blah blah..” For those following @marketsmuse, there’s no 20-20 hindsight; our resident pundits (with trading market pedigrees that go back to the 1980’s) have been shouting “Caution Ahead!!” for at least 4 months. (see the pinned tweet). But, who wants to listen to experienced (if not cynical) professionals who have lived through multiple market cycles, especially when prices keep going up? Who wants to risk taking a profit and paying taxes on those gains when the asset value keeps going up, with or without fundamental justification? The answer: people who are (i) naïve (ii) overly-optimistic (iii) financially irresponsible (iv) not old enough to appreciate that what goes up, must go down.

Whatever black swans have been flying over head for the past 6 months, now that equity prices have suffered multiple-day declines of 1%-3% (and the interim 1%-2% “dead cat bounce”) we need to blame someone!! After all, our very own president has been unwavering in his leadership mantra: “When the shit hits the fan, blame someone else for the problem!”

Before the ink was dry on the famous Michael Lewis book “Flash Boys,” which profiled the May 2010 stock market crash, everyone knew who to blame. Before the first 1000 copies of that book left Barnes & Noble, government officials and regulators were busy sending out outlook meeting invites to the primary suspects-the heads of HFT proprietary trading firms that had come to dominate the trading of shares in US companies listed on public exchanges (and ‘dark venues), as well as stock index futures traded on electronic venues in Chicago.

Rules were introduced. Market structure lobbying groups were formed. Exchange executives pilot tested uptick rule changes. Fintech firms that provided ‘better solutions’ now represent more than just a cottage industry as evidenced by the fact, three of the leading HFT firms have through acquisition, become the three largest NYSE DMMs. For old folks, DMM is the contemporary phrase for ‘floor specialist’-the folks who are responsible for maintaining fair and orderly markets in the companies the NYSE assigns to market-makers on the floor of the NYSE. Pay-to-play and maker-taker rebate schemes advanced by brokers and exchange venues have flourished. Blah Blah Blah. Along the way, the US equities market, spurred by improving economic circumstances, and the last 10 years have been pretty much one long wet dream for traders and stock investors. The evolution of high-frequency trading morphed even more.

Irrespective of bull vs. bear views on individual stocks and stock indices and the 1500+ Exchange-Traded Funds that provide thematic investing styles, more than a carload of institutional investment managers still agree on one simple fact: share price movements in individual companies and ETFs are exacerbated by high-powered black boxes that spit out millions of orders per minute. Those orders are often based on what has transpired in the markets during the past few seconds. This algorithmic approach to trading causes educated investors to scratch their heads when observing the value of shares in public companies can gyrate so violently in the course of an hour or a day, despite the fact those companies haven’t made any earnings report nor announced any positive or negative news as to the health of their business or the industry they sit in.

How does a company’s enterprise value move 10% down one day, then 5% up the next? Are there so many investors with differing views who are expressing these views constantly via buying and selling millions of shares? No. Honest electronic trading industry experts will estimate that at least 80% of the time, transactions taking place at the NYSE or NASDAQ are between two ‘transformers’; computer bots that are set on auto-trade. These black box powered bots do not represent investors, they don’t smoke (unless the computer is overheated and not residing in a freezer), they don’t curse and they don’t sweat—they simply spit out–orders based on algorithms.

Put more simply, actual investors are not involved in upwards of 90% of the trades taking place. Bottom line: the exaggerated changes in publicly traded corporate enterprise values that take place from second to second are even more pronounced as prices move lower. That’s a real fact, not a Kelly Ann Conway or Sarah Huckabee-style “alternative fact.” More than a handful of objective market observers and participants have long argued that Wall Street has evolved into a Battle of the Transformers”; price moves and volatility are powered by computers, not by momentary sentiment changes on the part of real investors.

But, we live in a blame game world, as best evidenced by our so-called leaders (yes, we’re referring to the current occupant of the White House) who, when faced with obstacles or after making stupid decisions, automatically blame others for the disaster that occurred recently. And those blames are applauded by the blind mice and sheep who go along with the stupid decisions made for them.

Because our pundits have accurately predicted this latest market down draft, allow us to further predict that we want to be “long on” private jet services to Washington (NYSE: BRK.A) and we’d love to invest in engagement contracts issued by Wall Street-friendly PR Crisis Management guru. Those folks will be on speed dial for the best-known HFT honchos, starting yesterday. Caveat Emptor: PR crisis management should be advanced by smart folks, not those trained in the art of jibber jabber and deflection. If there is a fundamental flaw, acknowledge it and implement transparent steps that will appease the plaintiffs and provide real solutions to the ‘problem’ .

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor via cmo@marketsmuse.com

Trifecta Month for GTS; NYSE DMM, Quant-Trading Powerhouse and Fin-Tech Think-Tank Now Aligned With Investment Bank Specializing in Primary Debt & Equity Capital Markets

GTS, the NYSE’s Top DMM, and one of the global trading market’s leading multi-asset electronic market-makers, is on a strategic deal-making binge. On the heels of GTS co-founder and CEO Ari Rubenstein’s November 2 announcement that his firm acquired Cantor Fitzgerald’s 35-member ETF market-making and institutional broking crew, last Thursday while in London, Rubenstein announced that GTS is expanding its collaboration with BNP Paribas to now include live-streaming US equities pricing, on top of already delivering GTS’s UST price feed through BNP’s platform. Making November a hat-trick month for GTS, Rubenstein today announced that his firm is joining forces with boutique investment bank Mischler Financial Group (“Mischler”), a specialist in primary debt and equity capital markets and institutional brokerage providing secondary market execution for equities and fixed income.

Founded in 1994, Mischler Financial is also the industry’s oldest diversity firm owned and operated by service-disabled veterans; a designation that enables GTS to advance a Diversity & Inclusion (D&I) value-add to its armory of new solutions and client experience that GTS will bring to investment managers and issuers of debt and equity across the listed-company landscape.

Below is the opening extract of the press release.

New York, NY – November 19, 2018 – GTS, the New York Stock Exchange’s largest Designated Market-Maker (“DMM”) and a leading electronic trading firm, and Mischler Financial Group, Inc. (“Mischler”), the financial services industry’s oldest minority broker-dealer owned and operated by service-disabled veterans, today announced a strategic alliance that will establish a best-in-class offering for primary debt and equity market underwriting as well as secondary market best execution across the capital markets.

The partnership, which is anchored by a technology-powered offering for public companies and a broad universe of capital markets participants, will yield a low-cost, more efficient and more effective trade execution experience. Mischler will become a “forward operating base” for the growing GTS capital markets franchise, affording clients access to technology and sources of liquidity that are generally only available to the world’s most sophisticated investors.

Founded in 2006 as a proprietary, quantitative trading firm, GTS is now a recognized thought-leader in market structure and proudly oversees trading for more than one-third of NYSE-listed companies. The firm has an extensive track record developing and deploying proprietary, industry-best technology to bring better price discovery, trade execution and transparency to the markets.

“This is a high-tech, high-touch partnership designed to meet the needs of a new generation of issuers, asset managers, and trading and investment professionals seeking low-impact market liquidity and best-in-class execution,” said Ari Rubenstein, Co-Founder and Chief Executive Officer of GTS. “Clients are rightfully demanding innovation in the marketplace, and this alliance is uniquely designed to provide that and much more.”

Mischler, established in 1994, is an active underwriter across global equities, corporate and municipal debt, government securities and structured products. In the last three years alone, Mischler has played a role in almost 700 primary debt and equity market transactions. The firm also provides conflict-free share repurchase services for corporate treasurers as well as secondary market trade execution in equities and fixed income for a discrete universe of public plan sponsors and institutional investment managers.

If you’ve got a hot insider tip, a bright idea, or if you’d like to get visibility for your brand through MarketsMuse via subliminal content marketing, advertorial, blatant shout-out, spotlight article, news release etc., please reach out to our Senior Editor via cmo@marketsmuse.com

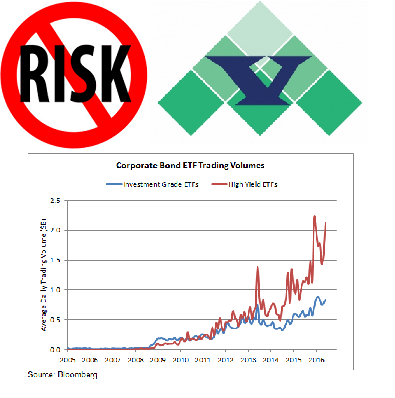

Virtu Says NO to Corporate Bond ETF risk-taking; Top Market-Maker Opines “Unable to Hedge ETF Constituents Due To Limited Liqudity”

During the better part of three years, MarketsMuse Fixed Income curators have often pointed to concerns expressed by market professionals who argue that the unfettered growth of corporate bond ETFs are masking the inevitable likelihood that once interest rates begin to rise, buy side fund managers fearful of mark-downs in their corporate bond positions will push the ‘sell button’ en masse to limit the P&L hit. Those in the camp expressing such concerns, which includes Virtu Financial, one of the most successful electronic market-makers in the industry, believe that such a mass exodus will wreak havoc on the now $8.4 trillion US corporate bond ecosystem* (*data according to Sifma), where new issuance for 2016 has just surpassed 1 Trillion dollars, and is a marketplace that since 2011 alone, has grown nearly 50% in terms of notional value and number of outstanding issues.

Per one senior market risk expert familiar with the thinking at Virtu, “Their’s isn’t simply a view typically attributed to academics, who have increasingly warned and have been equally derided by ETF lobbyists for suggesting a secondary market meltdown in corporate bond ETF products is inevitable when rates rise. Instead, Virtu has concluded that for those who make a business of ‘taking the other side’ of corporate bond exchange-traded funds, whether investment grade (e.g $LQD) or high yield themed (e.g $HYG), will find themselves playing a game of musical chairs, but there will be no chairs available for anyone when the music stops and traders will find themselves unable to find any liquidity in the respective ETF underlying constituents.”

Below opening excerpt from mainstream media outlet Bloomberg LP and reported by Bloomberg reporter Annie Massa:

One of the world’s largest electronic market makers won’t touch increasingly popular corporate bond ETF products because the underlying securities are too hard to trade.

Although New York-based Virtu Financial Inc. buys and sells everything from stocks to government bonds and futures on more than 235 exchanges around the world, it shuns products linked to corporate bonds like the $15 billion iShares iBoxx $ High Yield Corporate Bond ETF. The reason, according to Chief Executive Officer Doug Cifu, is that it’s too hard for Virtu to precisely hedge the trades.

“It’s definitely concerning you don’t have full and unfettered access to the underlying,” Cifu said, speaking at a Security Traders Association conference in Washington on Thursday. “That’s troubling.”

During the fourth quarter of 2015, TABB Group interviewed key US corporate bond market participants across buy-side, sell-side and specialized trade service providers.Across all segments covered within the survey, participants’ responses reflected dim expectations for liquidity available in the US corporate bond market for 2016. Apart from the threat of a “large scale macro crisis,” the most serious threat that participants identified was the ongoing decline in immediacy (balance sheet) provided by dealers.

Worldwide assets in bond ETFs have surged in recent years, jumping fivefold since January 2010 to about $600 billion, according to data compiled by Bloomberg. About 88 million shares of fixed-income ETFs have traded daily in the U.S. during the past 30 days, according to data compiled by Bloomberg.

Other market makers including Citadel Securities and Susquehanna do trade the ETFs, but Virtu’s absence is notable given how dominant the company is in other areas. Cifu said Virtu does trade ETFs containing U.S. Treasuries, including the ProShares UltraShort 20+ Year Treasury.

Virtu’s strategy involves arbitraging price difference in related assets, quickly entering and exiting the positions. With fixed-income ETFs, the company is concerned it can’t get access to the related bonds fast enough. Market makers with longer trading time frames may be less reluctant. Virtu’s line of thinking echoes worries elsewhere in the industry. Shares of the funds are often easier to trade than their underlying bonds, potentially posing a risk if there’s a sudden rush for the exit.

(Bloomberg) — Regulators could stem the migration of U.S. equity trading to dark pools by coordinating a cut in trading fees, an action exchanges are unlikely to take on their own, according to one of the biggest high-frequency firms.

Most exchanges are charging traders too much — 30 cents per 100 shares — pushing transactions off public markets to lower-cost private platforms such as dark pools, said Chris Concannon, an executive vice president at Virtu Financial LLC in New York. Regulators should review enacting a blanket reduction of the fees, which would also curb the rebates exchanges pay traders who facilitate transactions, he said.

The system of charging investors for trades while paying brokers, a model known in the industry as maker-taker, is common at the majority of U.S. stock exchanges after market making by humans became less profitable over the last decade. While these pricing systems probably can’t be dismantled, there are “things you can regulate to mitigate their impact on market structure,” Concannon said during an interview.

For the entire article, including compelling counter-points made by other industry veterans, please click here .

Virtu Financial LLC said it bought a Dutch market-making business, bolstering the U.S. trading firm’s presence in a European exchange-traded-funds market that has emerged as a profitable battleground for high-speed traders.

Virtu, one of the most-active traders of stocks, commodities and other securities in the U.S. and Europe, acquired the market-making division from Amsterdam-based Nyenburgh Holding BV, the companies said. They declined to disclose the value of the transaction.

Market makers stand ready to buy and sell securities at quoted prices, helping ensure that trades are executed smoothly. Market makers take a sliver of profit from each transaction, and the flow of data can help them profit in their own trades.

With the Nyenburgh deal, New York-based Virtu gains relationships with ETF issuers as well as buyers and sellers of the instruments, which include pensions and hedge funds, said Chris Concannon, a Virtu partner and chief compliance officer of its broker-dealer operation. Virtu has traded European ETFs since 2009.

Virtu expects growth in the ETF market will help fuel trading in the assets that underlie them, from gold and palladium to agricultural-commodity futures. The firm, through its Dublin-based office, became a registered market maker on the London Stock Exchange in August, and is registering on major European exchanges, said Douglas Cifu, Virtu’s president and chief operating officer.

The deal comes amid mounting competition and regulation in the European market for ETFs, or investment funds that track the performance of indexes and other baskets of individual securities. Unlike in the U.S., the majority of ETF trading in Europe occurs in over-the-counter transactions. But new rules are pushing more ETF trading onto exchanges, providing opportunities for trading firms like Virtu to grab a bigger share of the market.

Noted James Ryan of London-based ETF broker WallachBeth International, “Virtu’s expanded role as a liquidity provider in European-based ETFs will necessarily enhance the playing field as the ETF market in Europe continues to evolve and otherwise catch up to the US market in terms of both institutional investor transparency and overall liquidity.” Continue reading →

Shall we guess whether the 6-pack banks and their first cousins–the industry’s legacy source of liquidity to buy-side managers navigating the corporate bond market landscape are (i) happy to have a new competitor, (ii) happy not to have to make markets and tie up balance sheets with inventory of hard-to-move corporate bonds or (iii) f–king pissed that tech-focused prop trading firms are now invading a secondary market product area that banks have viewed as their exclusive territory since time began?

Shall we guess whether the 6-pack banks and their first cousins–the industry’s legacy source of liquidity to buy-side managers navigating the corporate bond market landscape are (i) happy to have a new competitor, (ii) happy not to have to make markets and tie up balance sheets with inventory of hard-to-move corporate bonds or (iii) f–king pissed that tech-focused prop trading firms are now invading a secondary market product area that banks have viewed as their exclusive territory since time began?